The gap usually surfaces one of two ways. At quarter-end, someone pulls the liability report, compares it to what cleared the bank, and finds a number that doesn't reconcile. Or it waits until year-end, when W-2 totals get pulled against state filings and a handful of states don't tie: a jurisdiction where the W-2 liability is $18,000 higher than what the state account reflects, or a filing that ran at the wrong rate for three quarters because a rate update never got applied.

The instinct in both cases is to treat it as a math error. Find the bad formula, rerun the totals, reconcile the spreadsheet. That instinct almost always leads somewhere frustrating, because the gap isn't in the spreadsheet. It's in the payroll system, in the state account, or in the space between what was filed and what the state actually received.

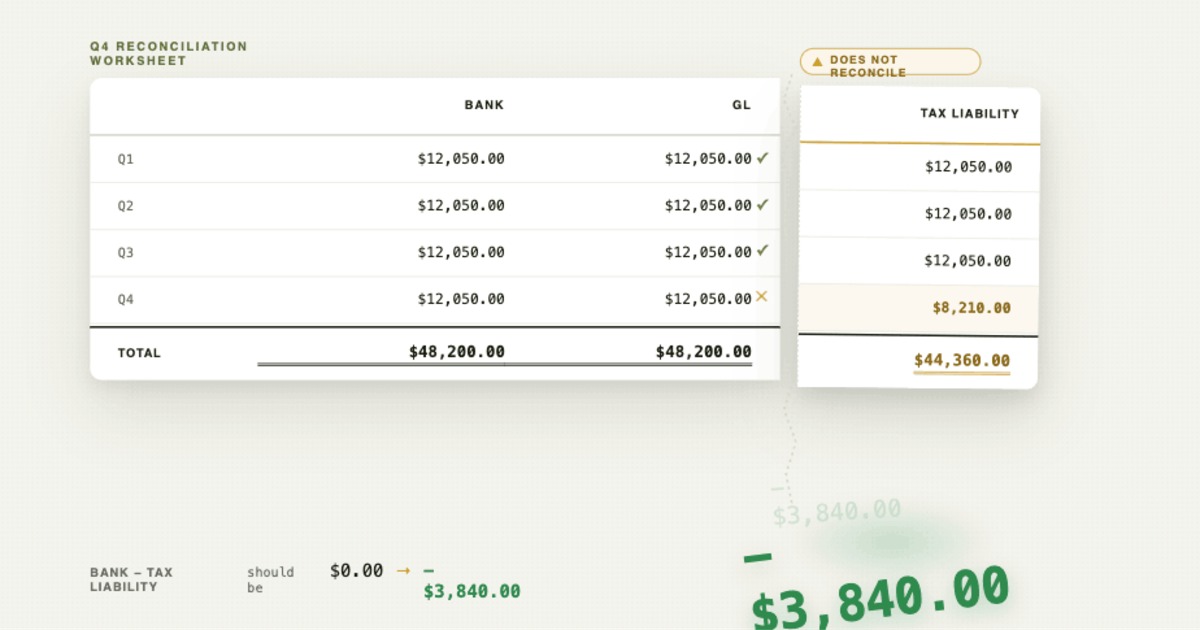

Payroll tax reconciliation gaps are compliance signals. Whether they surface at quarter-end or year-end, they tell you something broke upstream, usually weeks or months before anyone noticed.

Why Payroll Tax Numbers Don't Match

Most mismatches trace back to one of four places, and they're rarely independent.

Rate changes that didn't propagate. A jurisdiction updated its withholding rate or wage base mid-year. The update was supposed to flow through automatically. It didn't. Filings went out at the old rate, and the variance compounds with each passing quarter across every affected employee.

Jurisdictions that processed but never filed. An employee was set up in a new state. Payroll ran correctly, the withholding amounts look right, but the state account was never properly established. The payroll system shows withholding. The state has no corresponding record.

Deposit timing and posting mismatches. A payment cleared the bank in one period and got posted to another. The GL shows it one way, the state account shows it another, and neither matches what the payroll system has on record. At quarter-end or year-end, three separate systems have three different answers for what was paid and when.

Quarterly filing errors that carried forward. A Q1 filing went out with an incorrect wage base. Q2 assumed Q1 was correct. By Q4 the accumulated error is material, and tracing it requires pulling four quarters of data across every affected jurisdiction.

What MasterTax Catches, and What It Doesn't

MasterTax is a calculation and filing engine. It produces correct outputs when it receives correct inputs, and it surfaces exceptions when what it expects to find doesn't match what it sees. Teams that run MasterTax well use those exception reports actively.

The structural limit is that MasterTax only knows what it's been configured to know. A jurisdiction that was never set up correctly doesn't appear in exception reports, because MasterTax wasn't configured to look for it. A rate that was applied incorrectly from day one generates no exception, because MasterTax has no external reference to check against. The absence of an alert is not confirmation of accuracy. It's confirmation that the system isn't looking for what it doesn't know about.

This is the garbage-in-garbage-out problem, and it shows up at every reconciliation point. MasterTax can show a clean internal record while a state account carries an outstanding balance, because MasterTax's view and the state's view are maintained separately and never compared in real time. That gap compounds quietly between quarters and becomes visible when the forcing function arrives.

The Three-Way Reconciliation That Doesn't Happen

The standard that prevents reconciliation surprises is a daily three-way check: what cleared the bank, what the GL recorded, and what the tax liability system shows. Those three numbers should tie every day, and when they don't, the variance gets investigated before it compounds.

Most companies don't run this. They reconcile at quarter-end, or at year-end when the W-2s force the issue. MasterTax touches only one of the three legs: the tax liability. The bank and the GL live in separate systems, and pulling them together into a real reconciliation is a manual exercise most teams don't have capacity to run regularly. "Quarter-end fire drill" is how one payroll director described it. The same team processing current payroll is also trying to reconstruct three months of data to understand why the numbers don't match.

The further back the error goes before it gets caught, the more it costs to fix.

What a Proper Reconciliation Actually Requires

The reconciliation that closes the gap isn't a spreadsheet exercise. It's a cross-system audit that needs to run on two cadences: quarterly to catch gaps before they compound, and annually to validate the full year against what states actually received.

The quarterly reconciliation. Before each set of returns goes out, run the three-way check across bank, GL, and tax liability. Pull each state account and confirm that what was deposited matches what was filed. Any variance that surfaces at this point is one quarter old, not four. Flag it, trace it, and correct it before moving forward.

The year-end W-2 reconciliation. Pull the W-2 totals by state and reconcile them against the aggregate of all four quarterly state returns for the same period. The withholding reported on W-2s should match what was reported to the states across the year. Where it doesn't, trace back quarter by quarter to find where the divergence started.

For both cadences, pull the state account transcript directly from each agency: what was received, when, and how it was applied. Cross-reference that against what was filed. Every variance gets logged and categorized: underpayment, overpayment, period mismatch, or unknown.

This process surfaces what MasterTax can't: the gap between what the system shows and what agencies actually have on record. There are over 15,000 payroll tax jurisdictions in the US, each tracking filings and payments independently, and none of them share data with your payroll system in real time. The IRS Publication 15 framework covers federal employer obligations, but the state-by-state reconciliation is where most of the exposure lives.

When the Numbers Don't Tie

A reconciliation variance, whether it shows up at quarter-end or year-end, isn't a spreadsheet problem waiting to be solved with the right formula. It's evidence that something in the upstream process broke: a rate wasn't updated, a jurisdiction wasn't established, a payment posted to the wrong period, or a quarterly filing doesn't match the W-2 it's supposed to support.

"It's a matter of when, not if it results in fees and penalties" is how one enterprise payroll leader described their exposure heading into year-end with unresolved variances. The correction window for quarterly returns and annual W-2 reconciliations isn't indefinite, and the further back the error goes, the more it costs to fix.

Purpose-built payroll tax compliance tooling maintains a continuous view of what was filed against what jurisdictions have on record, so reconciliation reflects daily comparison rather than a single quarterly scramble. For teams working through a backlog of open variances right now, Tax Pilot Advisory runs the cross-system audit, identifies what's open at the agency level, and manages the correction process through to resolution.

Running MasterTax without the in-house expertise to keep it current? Tax Pilot Advisory becomes your outsourced MasterTax expert. We handle the configuration, jurisdiction maintenance, and notice management so your team isn't filing blind between quarters. See how Tax Pilot Advisory works →

Building an in-house payroll system, or running on legacy tax software? Tax Pilot is a purpose-built payroll tax compliance platform replacing legacy tools like MasterTax. API-first, daily reconciliation, every state. Currently in beta with select customers. Request a demo →